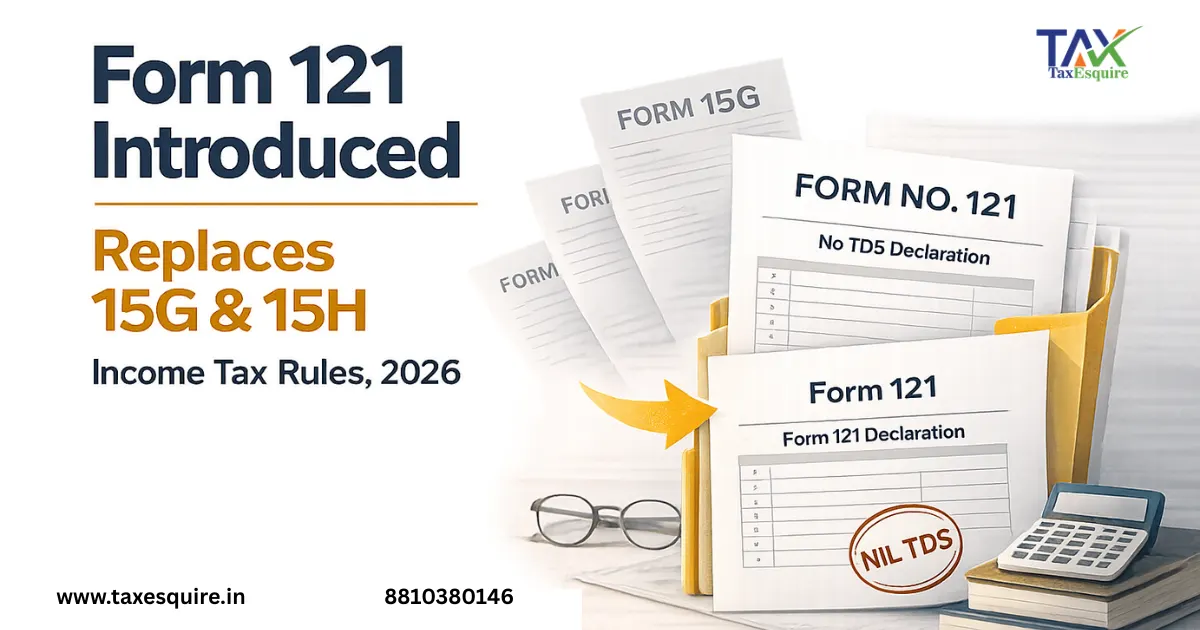

Form 121 Replaces 15G & 15H: New TDS Rule

Overview

Form 121 is a turning point for the Tax Deduction at Source system in India. Since the introduction of Form 121 instead of 15G and 15H, it has become imperative that one should have knowledge about this system so as to prevent themselves from any deductions of TDS in 2026.They lack information that is vital to the IT Deptt. and verifying that the taxpayer has filled out these forms with proper information is quite difficult.

Such an initiative is part of a larger digital tax structure initiated by agencies such as the Central Board of Direct Taxes.

Some of the firms in the present age allow the tax-payers to fill these forms online and they do not require the taxpayers to fill out these forms on a paper. It makes life easier for tax-payers but not for these firms or IT dept. because processing of these forms is largely paper based. In reality, these firms might be generating these forms based on online submission of details of the tax-payers and printing them on paper later.

Download Form121: Click here

What is Form 121 and Why It Matters

Form 121 is a single self-declaration form introduced under the Income-tax framework from FY 2026-27 onwards, replacing the earlier Forms 15G and 15H. Its primary objective is to enable eligible taxpayers to receive certain incomes without deduction of TDS, provided their overall tax liability for the year is nil.

Unlike the earlier system where separate forms were prescribed based on age, Form 121 simplifies compliance by offering one unified declaration applicable to all qualifying taxpayers.

Earlier:

● Form 15G → for individuals below 60 years

● Form 15H → for senior citizens

Now form 121 applies to all eligible taxpayers, regardless of age

This unified approach reduces confusion and ensures better compliance in the evolving digital tax environment.

Who is Eligible to File Form 121?

Form 121 can be submitted by resident taxpayers whose estimated income does not attract any tax liability. This includes:

● Resident individuals (including senior citizens)

● Hindu Undivided Families (HUFs)

● Certain trusts and other eligible assessees

The key factor is not the category of taxpayer, but whether the final tax payable after all deductions is zero.

Conditions for Eligibility

● Must be a resident in India

● Total tax liability for the year must be nil

● Declaration must be submitted before TDS deduction

● PAN is mandatory

Failure to meet any of these conditions may result in TDS being deducted as per applicable provisions.

Who Cannot File Form 121?

The following are not eligible:

● Non-residents (NRIs)

● Companies and partnership firms

● Individuals/entities (Taxpayers) whose income results in a positive tax liability

Difference Between Form 15G, Form 15H and Form 121

Form of Declaration under section 393(6) of the Income-tax Act, 2025 for receipt of certain incomes without deduction of tax summary comparison with old Form and section:

Format and Components of Form 121

Form 121 is structured into two key sections, capturing details of both the taxpayer and the deductor to ensure proper reporting and compliance.

Part A – Details of the Declarant

This section focuses on the taxpayer furnishing the declaration. It covers:

Basic Information:

- ● Full name, address, and PAN

- ● Residential status along with date of birth

- ● Contact details and relevant financial year

Income Particulars:

- ● Type and source of income

- ● Expected income for the year

- ● Total income from all sources

- ● Summary of income reported in the last two Income Tax Returns

Declaration:

A confirmation by the taxpayer stating that the overall tax liability for the year is nil, based on estimated income.

Part B – Details of the Payer

This section captures information about the person or institution responsible for making the payment.

Payer Information:

● Name and address of the deductor

● PAN and TAN details

● Contact information and applicable financial year

Declaration Records:

● Reference to declarant’s name, PAN, and UIN

● Nature and amount of income covered

● Date on which the declaration is received

Documents Required

To ensure smooth processing, taxpayers should keep the following ready:

● PAN card (mandatory)

● TAN details of the payer

● Proof of age (where relevant)

● Details of income and investments

● Bank account information

Steps to Fill Form 121

Filing Form 121 requires careful estimation and timely submission. The process generally involves:

Compute your total income for the year

Confirm that the final tax payable is zero after deductions

Obtain Form 121 from the Income Tax portal or the concerned institution

Fill in Part A with accurate personal and income details

Provide payer details, including TAN and institution name

Verify the declaration and submit it before any TDS is applied

Mode of Submission

Form 121 must be submitted separately to each payer from whom income is expected.

It can be furnished through:

● Physical submission (hard copy)

● Online mode via bank or financial institution portals

Timely submission is critical — the form should reach the payer before the income is credited, to avoid TDS deduction.

What Happens After Submission?

Once the form is received:

● The payer validates the details provided

● A Unique Identification Number (UIN) is generated for tracking

● Declarations are uploaded periodically to the Income Tax system

● The information is reported in quarterly TDS statements

Key Benefits of Form 121

- 1. Simpler Process: Only one form is required instead of two separate forms.

- 2. Greater Transparency: Digital verification reduces errors and mismatches.

- 3. Improved Financial Planning: Investors can better plan income without worrying about unnecessary TDS deductions.

- 4. Faster Compliance: Reduces paperwork and speeds up processing.

Important Points to Remember

Verify the authenticity of the taxpayer details in the declaration

Generate and assign a UIN for each submission

Upload the declarations monthly within prescribed timelines

Include such declarations in their TDS reporting framework

Report these declarations in quarterly TDS returns (Form 14Q)

Ensure PAN is mandatory for all declarations

Obtain a separate form for each payer

Accept declarations valid only for one financial year

Ensure that income is still reported in the ITR by the taxpayer

Be cautious, as false declarations may lead to penalties

Practical Illustration

Consider a taxpayer with an annual income of ₹2.5 lakh, which includes ₹40,000 earned as interest.

Earlier Approach: The taxpayer would have submitted Form 15G to avoid TDS on the interest income.

Revised Approach (from 2026 onwards):The same taxpayer will now furnish Form 121, replacing the earlier forms.

Outcome: No tax is deducted at source, as the overall tax liability remains nil, the process becomes more streamlined with a single, standardised declaration form across taxpayers

Impact on Taxpayers and Investors

● Easier compliance

● Reduced paperwork

● Better tracking through digital systems

● Helpful for FD and bond investors

● Minimizes need for tax refunds

Common Mistakes to Avoid

● Submitting form after TDS deduction

● Incorrect income estimation

● Not quoting PAN

● Submitting to only one payer

Conclusion

Form 121 is a significant step toward simplifying India’s TDS system. By replacing Forms 15G and 15H, it introduces a single, efficient, and digitally aligned process for taxpayers.

For individuals with nil tax liability, Form 121 ensures no unnecessary TDS deduction, smoother compliance, and better financial planning. However, accuracy in filing and timely submission remain crucial to fully benefit from this system.

FAQS on form 121

Q1. What is Form No. 121 and its purpose?

Ans: Form No. 121 is a declaration submitted by a taxpayer stating that the tax on their estimated total income for the financial year will be NIL. Its purpose is to avoid deduction of tax at source (TDS). Once submitted to the payer, TDS will not be deducted on eligible payments.

Q2. Has Form No. 121 replaced Forms 15G & 15H?

Ans: Yes, Form No. 121 has replaced Forms 15G and 15H. Now, both taxpayers below 60 years and senior citizens (60 years and above) can use a single form to declare NIL tax liability and avoid TDS.

Q3. What types of income are covered under Form No. 121?

Ans: The declaration covers various incomes such as:

● PF withdrawals and pension

● Insurance commission

● Rent income

● Interest on deposits

● Income from mutual funds

● Life insurance policy payments

● Dividend income

Q4. Is filing Form No. 121 mandatory?

Ans: No, filing is not mandatory. It is optional and meant for taxpayers whose estimated total income for the year is NIL and who want to avoid TDS. The declaration must be submitted separately for each financial year.

Q5. Who is eligible to use Form No. 121?

Ans: Eligible taxpayers include:

● Resident individuals (below and above 60 years)

● Hindu Undivided Families (HUFs)

● Other specified eligible entities

Not eligible:

● Companies and partnership firms

● Non-residents

Q6. Is Form No. 121 required to be submitted to each payer?

Ans: Yes, the taxpayer must submit the declaration (Part A) separately to each payer responsible for making the payment.

Q7. Is PAN mandatory for Form No. 121?

Ans: Yes, quoting PAN is mandatory. If PAN is not provided, the declaration becomes invalid and TDS will be deducted at applicable rates.

Q8. What is the time limit for submitting Form No. 121?

Ans: The declaration must be submitted to the payer before the payment or credit of income (i.e., before the transaction date).

Q9. What are the modes of submission for Form No. 121?

Ans: The form can be submitted:

● In physical (paper) form

● Online (if the payer provides such a facility)

Q10. How does the payer submit Form No. 121 to the Income Tax Department?

Ans: The payer must submit the details electronically (Part B) on the Income Tax Department’s e-filing portal.

Q11. Are payers required to report transactions where TDS is not deducted?

Ans: Yes, such transactions must be reported in the quarterly TDS return in Form No. 140.

Q12. If income is received from multiple payers, is separate submission required?

Ans: Yes, the taxpayer must submit Form No. 121 separately to each payer.

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.