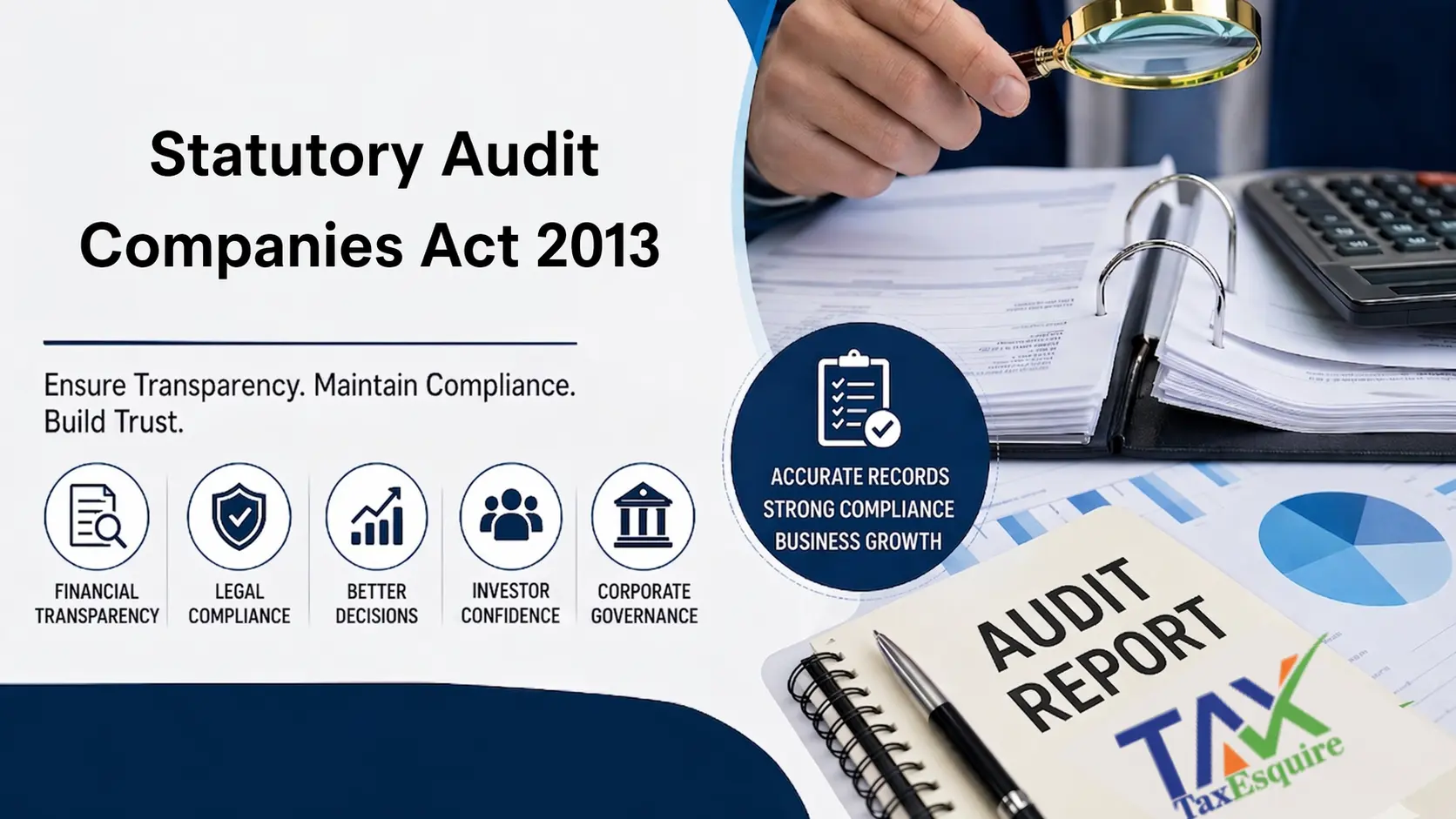

Statutory Audit Applicability Explained Under Companies Act 2013

Introduction

Running a company in India comes with plenty of legal and regulatory responsibilities, and one of the key ones is the statutory audit. According to the Companies Act, 2013, every registered company whether it is a Private Limited Company, Public Limited Company, or even a One Person Company (OPC) is required to go through this audit every financial year, no exception’s.

What makes it unique is that, unlike other type’s of audits that may depend on your turnover, profit, or specific business activitie’s, a statutory audit is mandatory no matter the size, revenue, or operational status of the company. Even if your company has zero transactions or is not earning a penny, you’ll still need to check this off your list each year!

The main goal of a statutory audit is to make sure:

● Financial transparency

● Accuracy of financial statements

● Legal compliance

● Trust among stakeholders

In simple terms, it acts as a financial health check-up for a company.

What is a Statutory Audit?

A statutory audit is a legally mandated independent examination of a company’s financial record’s, conducted by a practicing Chartered Accountant (CA).

The auditor evaluates whether:

● Books of accounts are properly maintained

● Financial transaction’s are accurately recorded

● Financial statement’s comply with accounting standard’s

● The Balance Sheet and Profit & Loss Account present a true and fair view

After completing the audit, the auditor issues an audit report, which is a formal opinion on the company’s financial position.

This report is essential for:

● Shareholders

● Investors

● Banks & financial institutions

● Government authorities

Legal Framework Governing Statutory Audit

Statutory audits in India are governed by the Companies Act, 2013, along with auditing standard’s issued by the Institute of Chartered Accountants of India (ICAI).

Key sections include:

● Section 139 – Appointment of Auditor

● Section 140 – Removal/Resignation of Auditor

● Section 141 – Eligibility, Qualifications & Disqualifications

● Section 143 – Responsibilities and Authority of an Auditor

● Section 145 – Signing of Audit Report

● Section 147 – Penalties for Contravention

These provisions ensure that audits are conducted with independence, transparency, and accountability.

Applicability of Statutory Audit

Statutory audit is mandatory for all companies, including:

● Private Limited Companies

● Public Limited Companies

● One Person Companies (OPC)

● Small Companies

● Dormant Companies

Important Clarification:

A statutory audit is required even if:

● The company has zero turnover

● There are no business transactions

● The company is inactive or dormant

Applicability for LLPs (Comparison)

Unlike companie’s, Limited Liability Partnerships (LLPs) are required to conduct an audit only if:

● Turnover exceeds ₹40 lakh, or

● Contribution exceeds ₹25 lakh

Types of Audits

While statutory audit is mandatory, companie’s may also be subject to other audits depending on their nature and size:

● Internal Audit – Focuses on internal control’s and operational efficiency

● Tax Audit – Applicable under the Income Tax Act based on turnover limit’s

● GST Audit – Applicable in specific GST cases or departmental audits

● Cost Audit – Applicable to certain industries for cost records

● Secretarial Audit – Ensures compliance with corporate laws

Appointment of Auditor

First Auditor

● Must be appointed within 30 days of incorporation

● Appointed by the Board of Directors

● If the Board fails, shareholders must appoint within 90 days

Subsequent Auditor

● Appointed at the Annual General Meeting (AGM)

● Hold’s office for 5 consecutive years (till the 6th AGM)

● Appointment is filed with ROC using Form ADT-1

Eligibility Criteria

● Must be a practicing Chartered Accountant or CA firm

● Should not have any conflict of interest

● Must meet independence requirements under the Act

Step-by-Step

The statutory audit process follow’s a structured approach:

1. Appointment of Auditor

2. Planning & Risk Assessment

3. Collection of Financial Data

4. Verification of Books of Accounts

5. Testing Transactions & Supporting Document’s

6. Evaluation of Internal Controls

7. Compliance Check with Law’s & Standard’s

8. Preparation of Audit Report

9. Submission of Audit Report

The auditor ultimately provide’s an opinion on whether the financial statements are free from material misstatements.

Due Dates & Compliance Timeline

Timely compliance is essential to avoid penaltie’s.

Key Deadlines:

● Financial Year End: 31st March

● Audit Completion: Before AGM

● AGM Deadline: Within 6 months from FY end (generally 30th September)

● ROC Filing:

○ Form AOC-4 – Within 30 days of AGM

○ Form MGT-7 – Within 60 days of AGM

Failure to meet these deadlines can lead to heavy penalties and additional fees.

Documents Required for Statutory Audit

To ensure a smooth audit process, companies must maintain proper records such as:

● Books of accounts

● Financial statements (Balance Sheet & P&L)

● Bank statements

● Purchase & sales invoices

● GST returns

● TDS returns and records

● Fixed asset register

● Statutory registers

● Board meeting minutes

● Previous audit reports

Benefits of Statutory Audit

Although mandatory, statutory audits provide several valuable benefit’s:

1. Financial Transparency: Ensures accurate and reliable financial reporting.

2. Builds Investor Confidence: Enhances credibility among investor’s, bank’s, and stakeholder’s.

3. Detection of Errors & Fraud: Identifies discrepancie’s, fraud risks, and irregularitie’s.

4. Better Decision-Making: Provide’s management with reliable financial insights.

5. Legal Compliance: Ensures adherence to regulatory requirements and avoids legal complications.

6. Improved Financial Discipline: Encourages proper record keeping and accountability.

Penalties for Non-Compliance

Non compliance with statutory audit requirement’s can lead to serious consequence’s under the Companies Act, 2013.

Penalties Include:

● Company penalty: ₹25,000 to ₹5,00,000

● Auditor penalty: ₹25,000 to ₹5,00,000

● Additional fines for continuing default

Other Consequences:

● Legal proceedings

● Director disqualification

● Difficulty in raising fund’s

● Loss of business credibility

Common Mistakes Companies Make

Many companies face audit issues due to avoidable mistakes:

● Delay in appointing auditor

● Poor or incomplete documentation

● Missing compliance deadlines

● Lack of professional guidance

● Ignoring inactive company compliance

Avoiding these mistakes ensures a smooth and hassle-free audit process.

Why Choose TaxEsquire?

At TaxEsquire, we offer comprehensive statutory audit service’s designed to ensure complete compliance and peace of mind:

● Experienced CA

●

End-to-end audit and ROC filing

support

Timely completion and compliance

Accurate financial analysis

Transparent and affordable pricing

We help businesses stay compliant while focusing on growth.

Conclusion

Statutory audit under the Companies Act, 2013 is not just a legal formality it is a critical component of corporate governance. It ensures that financial statements are:

● Accurate

● Transparent

● Legally compliant

Whether your company is active, inactive, small, or growing, statutory audit is mandatory and essential. By partnering with experienced professionals like TaxEsquire, businesses can ensure smooth compliance, reduced risk, and enhanced credibility.

Author: CA POONAM GUPTA & ADV LOKESH GUPTA

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.