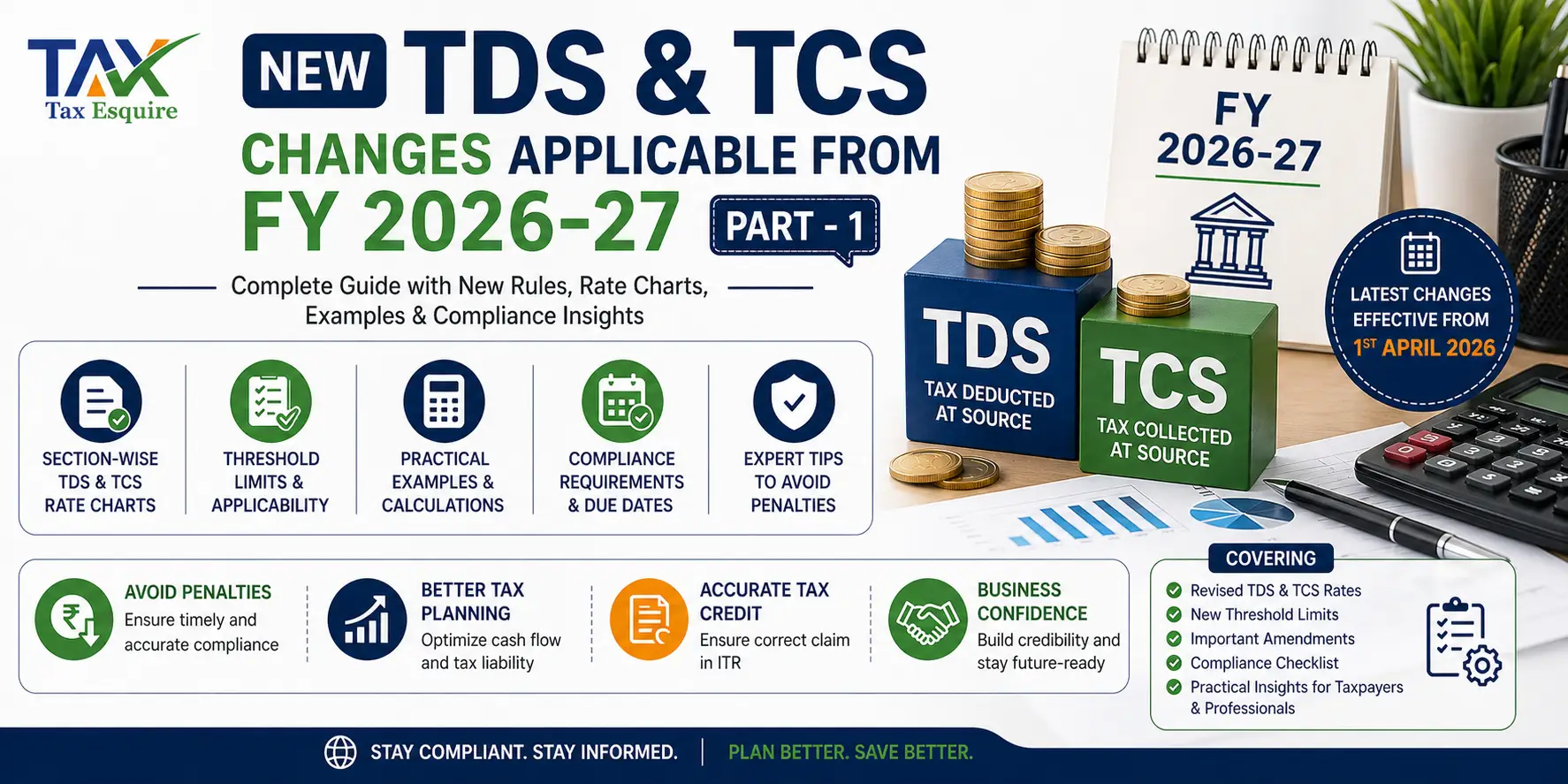

New TDS & TCS Changes Applicable from FY 2026-27 - Part 1

Introduction

Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) are foundational pillars of India’s direct tax system. These mechanisms ensure real-time tax collection, reduce tax evasion, and improve financial transparency across the economy.

With the introduction of revised provisions aligned with the Income Tax Act, 2025, effective from April 1, 2026, there are important updates in rates, thresholds, compliance procedures, and reporting standards.

This comprehensive guide is designed for businesses, professionals, accountants, and taxpayers, offering a complete understanding of TDS & TCS rates for FY 2026–27, along with practical insights and expert guidance.

What is TDS (Tax Deducted at Source)?

TDS is a mechanism where tax is deducted at the time of making specified payments such as salary, interest, rent, commission, or professional fees. The deducted tax is then deposited with the government.

Key Characteristics:

Deducted before payment is made

Applicable on income generation stage

Responsibility lies with the payer (deductor)

Credit is reflected in the recipient’s Form 26AS

Purpose of TDS:

Ensures steady revenue flow for the government

Minimizes tax evasion

Distributes tax burden throughout the year

What is TCS (Tax Collected at Source)?

TCS is the tax collected by the seller from the buyer at the time of sale of specified goods or transactions.

Key Characteristics:

Collected at the time of sale

Applicable on specified goods/services

Responsibility lies with the seller (collector)

Common Transactions Covered:

Sale of scrap, minerals

Sale of goods exceeding threshold

Foreign remittances (LRS)

Overseas tour packages

Purpose of TCS:

Tracks high-value transactions

Expands tax base

Improves transaction transparency

Key Changes in TDS & TCS from April 2026

The financial year 2026–27 introduces structural refinements aimed at simplification and digitization:

Major Updates:

Rationalization of threshold limits

Simplification of rate structures

Integration with AI-based compliance systems

Enhanced reporting & reconciliation requirements

Stricter penalties for defaults and delays

Impact:

Increased compliance for businesses

Improved transparency in transactions

Reduced ambiguity in tax deduction rules

TDS Rate Chart for FY 2026–27 (Section-wise)

Below is a simplified yet comprehensive overview:

Important Notes:

Higher rate applies if PAN is not available (Section 206AA)

Special rates apply for non-residents

Surcharge and cess may apply where relevant

TCS Rate Chart for FY 2026–27

Key Highlights:

Higher rates may apply in non-filing cases (Section 206CCA)

TCS credit can be claimed by the buyer during ITR filing

TDS Threshold Limits for FY 2026–27

Threshold limits determine when TDS becomes applicable.

Key Insights:

No TDS if payment is below prescribed limit

Limits apply per transaction or annually, depending on section

Aggregation rules may apply

Example:

If contractor payment is:

₹25,000 → No TDS

₹35,000 → TDS applicable

TCS Threshold Limits & Applicability

Applicability Rules:

Triggered when sales exceed specified threshold

Seller must collect tax at time of receipt

Example:

If total sales exceed ₹50 lakh:

TCS @0.1% applies on amount exceeding ₹50 lakh

Major Sections Covered (Important Provisions Explained)

Understanding the key sections under TDS and TCS is crucial because each section applies to a specific type of transaction, and incorrect classification can lead to penalties or disallowances.

Section 192 – TDS on Salary

This section governs TDS on salary payments made by an employer to an employee.

Key Features:

TDS is calculated based on applicable income tax slab rates

Employer must consider:

Employee’s total income

Deductions (80C, 80D, HRA, etc.)

Chosen tax regime (old vs new)

Important Points:

No fixed TDS rate — depends on income level

Adjustments allowed during the year

Employer is responsible for accurate computation

Practical Insight: Incorrect estimation may result in short deduction, leading to interest liability.

Read the rest in 'New TDS & TCS Changes Applicable from FY 2026-27 - Part 2'.