Wage Structure & PF Calculation in Uttar Pradesh (FY 2026–27)

A Practical Compliance Guide by TAX ESQUIRE

With changing laws and tighter enforcement , payroll compliance in India now demands precision—especially when it comes to minimum wages and Provident Fund (PF) calculations. For employers in Uttar Pradesh, understanding the correct wage breakup is essential to avoid non-compliance and financial exposure.

Whether you are a startup, SME, or large enterprise, understanding minimum wages, wage components, and PF applicability is essential to avoid penalties, litigation, and reputational risks. This comprehensive guide by TAX ESQUIRE explains everything you need to know for FY 2026–27 in a clear and practical format.

What Are Minimum Wages in Uttar Pradesh?

Minimum wages are the legally mandated lowest wages that employers must pay to workers. These wages are notified by the state government and are binding on all eligible establishments.

In Uttar Pradesh, minimum wages consist strictly of:

Basic Wage

Variable Dearness Allowance (VDA)

These two components together form the total minimum wage, and both are mandatory. Minimum wages are:

Calculated on a 26-day working basis

Revised twice a year (April & October) based on inflation

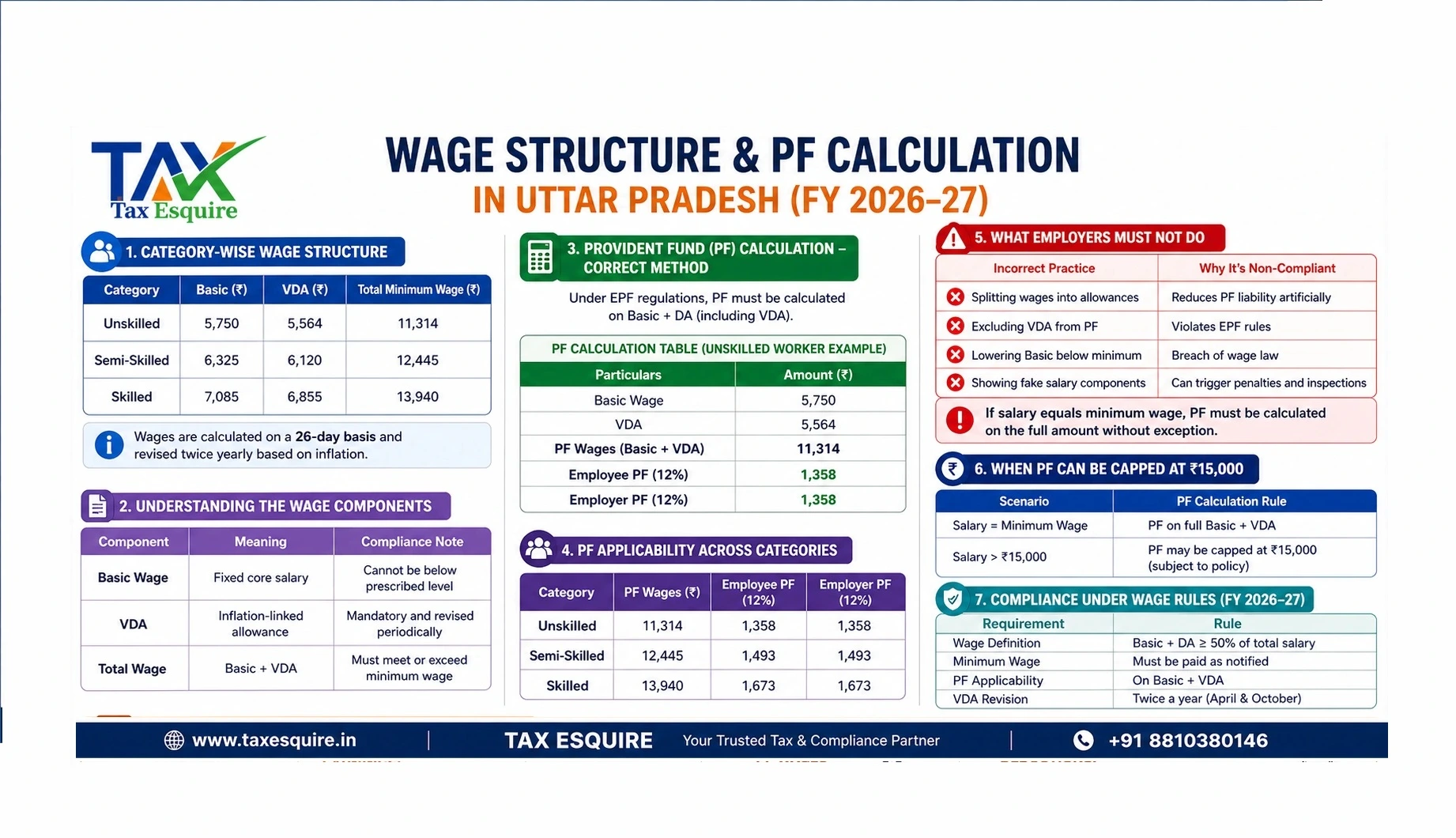

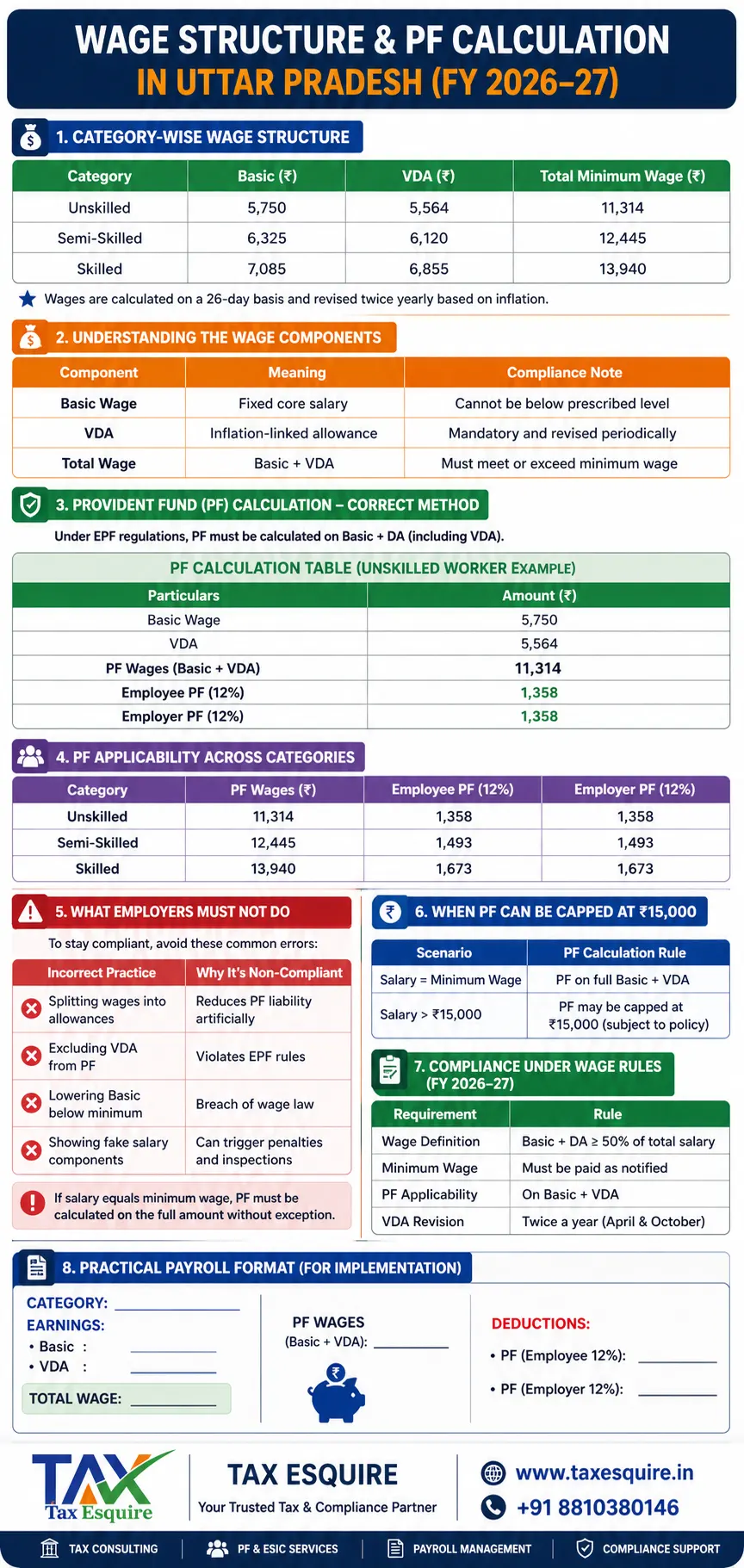

Minimum Wages – Uttar Pradesh (Effective April 2026)

Minimum wages in Uttar Pradesh consist strictly of Basic + Variable Dearness Allowance (VDA). These are statutory components and must be paid in full.

Category-wise Wage Structure

Understanding the Wage Components

Provident Fund (PF) Calculation – Correct Method

Under EPF regulations, PF must be calculated on Basic + DA (including VDA).

PF Calculation Table (Unskilled Worker Example)

PF Applicability Across Categories

Rule: If an employee is paid minimum wages, PF must be calculated on the full wage amount without exception.

What Employers Must Avoid

To stay compliant, avoid these common errors:

If salary equals minimum wage, PF must be calculated on the full amount without exception.

When PF Can Be Capped at ₹15,000

Employers can limit PF contributions to ₹15,000 only if the employee’s salary exceeds this threshold and proper policy documentation exists.

Compliance Under Wage Rules (FY 2026–27)

PRACTICAL PAYROLL FORM

For Implementation

Category: _______________________________

EARNINGS

Basic Salary: ____________________________

VDA: ____________________________

Total Wage: ____________________________

PF WAGES

PF Applicable Wages: ____________________________

DEDUCTIONS

PF (Employee 12%): ____________________________

PF (Employer 12%): ____________________________

NET PAY

Net Pay: ____________________________

Prepared By: ____________________________

Checked By: ____________________________

Date: ____________________________

Why Proper Wage Structuring Matters

A compliant payroll system offers multiple benefits:

Legal Protection: Avoid penalties, notices, and legal disputes.

Financial Accuracy:Prevents underpayment or overpayment of statutory dues.

Employee Trust: Transparent salary structures improve workforce confidence.

Audit Readiness: Ensures smooth inspections and documentation checks.

Final Takeaway from TAX ESQUIRE

Minimum wages in Uttar Pradesh are fully composed of Basic + VDA

PF must be calculated on the entire wage amount, not a reduced figure

Artificial structuring to reduce statutory liability can lead to serious compliance risks

A transparent and compliant payroll system protects both employer and employee interests

For businesses, the focus should not just be on salary disbursement—but on accurate structuring, statutory adherence, and audit readiness.

TAX ESQUIRE recommends periodic payroll reviews to ensure alignment with evolving labour laws and notifications.