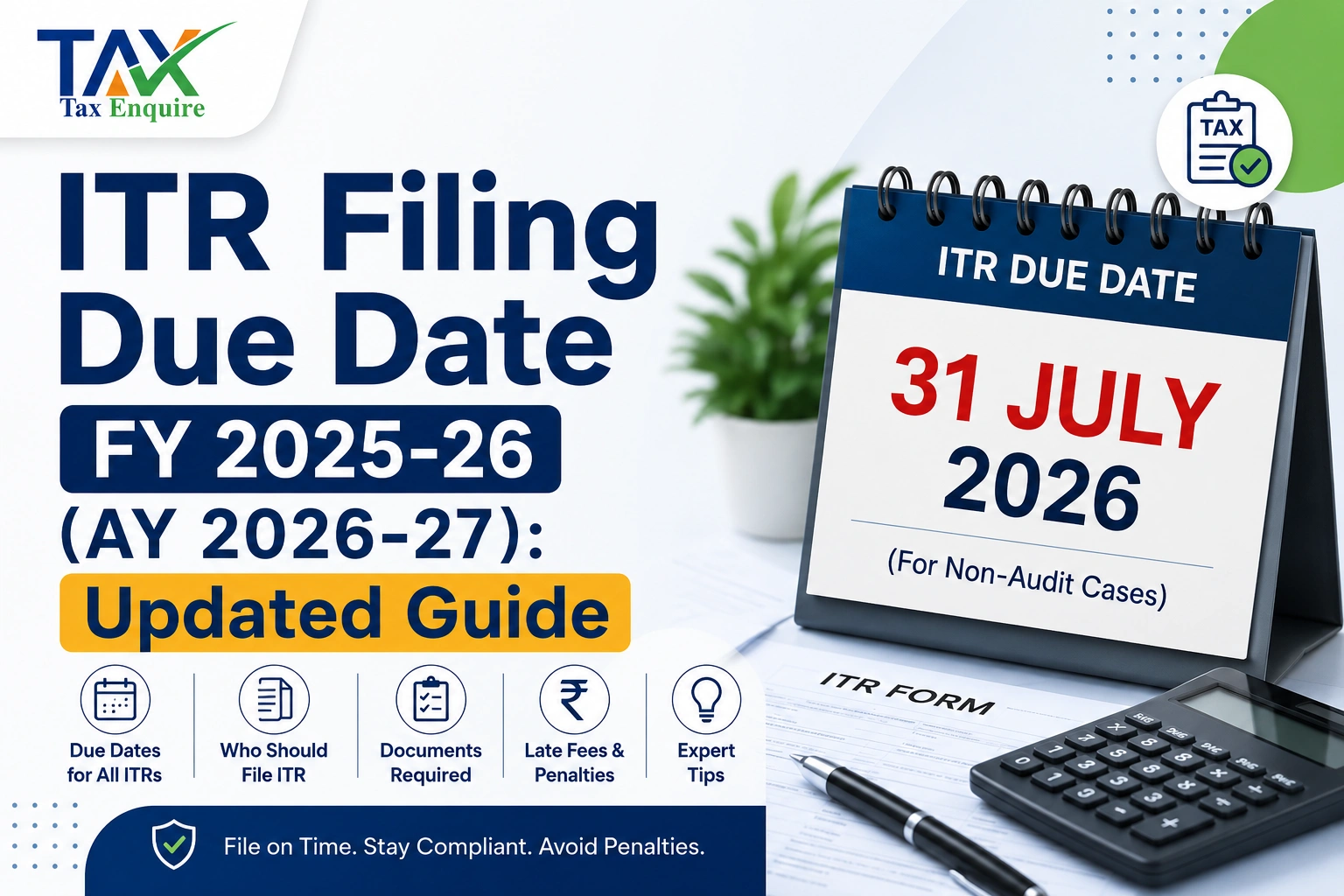

ITR Filing Due Date FY 2025-26 (AY 2026-27): Updated Guide

Filing Income Tax Return (ITR) within the prescribed due date is essential to avoid penalties, interest, notices, and loss of tax benefits. For Financial Year (FY) 2025-26 relevant to Assessment Year (AY) 2026-27, taxpayers must carefully understand the latest due dates, interest provisions, revised return timelines, and compliance updates.

The Income Tax Department has prescribed different due dates depending upon the category of taxpayer and audit applicability.

Important Update: Income Tax Act 1961 vs Income Tax Act 2025

Though the new Income Tax Act, 2025 is proposed to come into effect from 1 April 2026, the provisions of the Income Tax Act, 1961 will continue to apply for AY 2026-27 since the income pertains to FY 2025-26 ending on 31 March 2026.

Therefore, all provisions relating to:

Section 139

Section 234A/B/C

Section 234F

Section 44AB

Deductions under Chapter VI-A

will continue to govern ITR filing for AY 2026-27.

1. Major Updates in ITR Filing for AY 2026-27

1. Separate Due Dates for Different Non-Audit Taxpayers

One of the key compliance changes for AY 2026-27 is the distinction between

ITR-1 & ITR-2 taxpayers

ITR-3 & ITR-4 taxpayers

Now:

Salaried and simple non-audit taxpayers generally have due date of 31 July 2026

Business/profession non-audit taxpayers filing ITR-3 or ITR-4 may file up to 31 August 2026.

This change aims to reduce portal congestion and improve filing efficiency.

2. Revised ITR Forms Notified

CBDT has notified revised ITR Forms 1 to 7 for AY 2026-27 with additional disclosure requirements and compliance reporting.

Important updates include:

Reporting of long-term capital gains

Buyback loss disclosures

F&O and intraday trading details

Additional address reporting

Expanded prefilled information

Improved AIS/TIS reconciliation

3. Higher Focus on AIS & Compliance Matching

Taxpayers must now carefully reconcile the following:

Form 26AS

AIS (Annual Information Statement)

TIS (Taxpayer Information Summary)

TDS certificates

Mutual fund transactions

Stock market transactions

Foreign remittances

Mismatch may result in:

Defective return notices

Refund delays

Scrutiny notices

Demand notices

Who Should File ITR Even if Income is Below Taxable Limit?

Many taxpayers believe ITR filing is mandatory only when tax liability arises. However, return filing may still be compulsory in several cases.

You should file ITR if:

Total income exceeds basic exemption limit

TDS has been deducted

Foreign assets are held

High-value transactions are undertaken

Bank deposits exceed prescribed limits

Electricity expenses exceed specified threshold

Foreign travel expenses incurred

Business losses need carry forward

Refund claim is pending

Loan or visa documentation required

IF you missed filing the ITR on the due date, what should you do?

Then you have 2 options; they are

Belated Return and Updated Return

Revised Return under Section 139(5)

If any mistake is noticed after filing original ITR, taxpayer can revise return.

Common mistakes include:

Wrong bank account

Missed income disclosure

Incorrect deduction claim

Wrong ITR form selection

TDS mismatch

Omitted capital gains

Last date to revise return for AY 2026-27:

31 December 2026

Interest for Late Filing of ITR

Section 234A – Delay in Filing Return: Interest at 1% per month or part thereof is payable on outstanding tax liability if ITR is filed after due date.

Section 234B – Default in Advance Tax: Interest at 1% per month applies if advance tax paid is less than 90% of total tax liability.

Section 234C – Delay in Advance Tax Installments: Interest at 1% per month applies for deferment of quarterly advance tax installments.

Late Filing Fee under Section 234F

If return is filed after due date, late fees under Section 234F may apply.

Which ITR Form is Applicable for AY 2026-27?

Consequences of Missing ITR Due Date

Failure to file ITR within due date may lead to:

Interest under Sections 234A/B/C

Late filing fee under Section 234F

Delay in income tax refund

Loss of carry forward of business and capital losses

Higher chances of notices and scrutiny

Difficulty in loan or visa approval

Income Tax Act 1961 vs Income Tax Act 2025 – Section Comparison

Note: Proposed section mapping under Income Tax Act 2025 is subject to final implementation and notification.

Documents Required for ITR Filing

Salaried Individuals

PAN & Aadhaar

Form 16

AIS & Form 26AS

Investment proofs

Bank statements

Business & Professionals

Financial statements

GST returns

Audit reports

TDS certificates

Investors

Capital gain statements

Mutual fund reports

Dividend details

Benefits of Timely ITR Filing

Timely filing offers several financial and legal benefits:

Faster Refund Processing:Early filed returns generally receive quicker refund processing.

Easy Loan Approval: Banks and NBFCs frequently ask for:

2-3 years ITR copies

Computation of income

Acknowledgement receipts

Visa Processing:Many embassies require ITRs as proof of financial stability.

Carry Forward of Losses:Business and capital losses can generally be carried forward only if ITR is filed within due date.

Avoid Notices & Penalties: Timely and accurate filing reduces litigation and compliance risk.

Conclusion

For AY 2026-27, taxpayers should ensure timely filing of Income Tax Returns under the provisions of the Income Tax Act, 1961. With increased AIS-based monitoring and enhanced disclosure requirements, proper reconciliation and timely compliance have become extremely important.

Taxpayers should avoid last-minute filing and ensure accurate reporting of income, deductions, capital gains, and tax credits to prevent penalties, notices, and refund delays.

Frequently Asked Questions (FAQs)

What is the due date for salaried taxpayers for AY 2026-27?

31 July 2026.

What is the due date for tax audit cases?

31 October 2026.

Can I file belated return after due date?

Yes, up to 31 December 2026.

What is the late filing fee under Section 234F?

Up to ₹5,000.

What is the interest rate for late filing?

Generally 1% per month under Sections 234A/B/C.

Is Income Tax Act 2025 applicable for AY 2026-27?

No, AY 2026-27 continues under Income Tax Act, 1961.

Can I revise my ITR after filing?

Yes, revised return can be filed up to 31 December 2026.

Author: CA POONAM GUPTA & ADV LOKESH GUPTA

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.